5-Star Google Reviews

5-Star Google Reviews  170+ Lenders

170+ Lenders  30+ Years’ Experience

30+ Years’ Experience

Let to Buy is one of the most mis-structured mortgage strategies in the UK.

The mistake? Treating two mortgages as separate applications instead of one coordinated plan.

Without proper strategy, applications fail for predictable reasons:

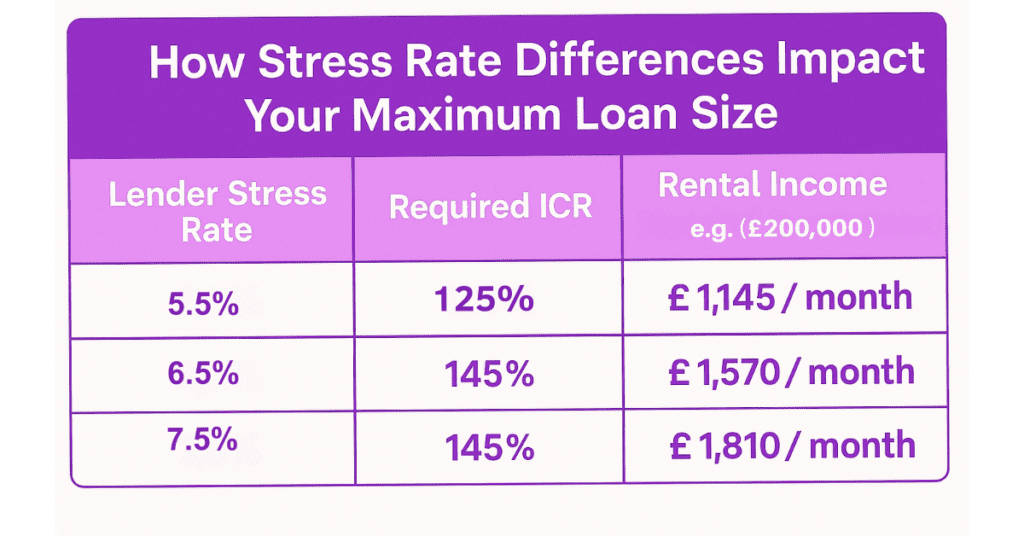

⚠️ Rental income failing ICR stress testing

⚠️ Overestimated rental projections

⚠️ Insufficient equity after valuation

⚠️ Residential affordability reduced by the Buy-to-Let commitment

⚠️ Dividend or bonus income assessed conservatively

⚠️ Lenders selected independently rather than as a compatible pair

If one lender declines, the onward purchase can be placed at risk.