⭐ 5-Star Google Reviews 🏦 170+ Lenders 📊 30+ Years’ Experience 🌍 UK-Wide Advice

SPV MORTGAGE ADVICE – OVERCOME LENDER BARRIERS AND BORROW MORE TAX-EFFICIENTLY

Specialist SPV mortgage advice using lender-approved, accountant-aligned structures to overcome ICR limits and unlock higher borrowing

Specialist Lenders

Discover Better Rates with Specialist Lenders to Grow Your Property Portfolio

Limited Company BTL Mortgages

Maximise Tax Efficiency & Secure Better Rates with Specialist Limited Company Mortgages

Mortgages for Complex Income

Get Approved Even with Irregular, Self-Employed or Multi-Source Income

Trusted by Landlords and Approved by Accountants

Real Reviews from Landlords Who Discover Expert Advice Aligned with Their Accountant’s Expectations

EXCELLENTTrustindex verifies that the original source of the review is Google. Lyndsey has been exceptional. Having a complicated case, Lyndsey was able to secure a mortgage for me. He kept me up to date throughout the whole process and has been extremely prompt with correspondence. Couldn't fault him at all. I highly recommend his services for anyone seeking a mortgage, especially those with extraordinary circumstances. Thank you very much.Posted onTrustindex verifies that the original source of the review is Google. Lyndsey (West Wales Money) helped me get a tricky mortgage deal through and was fast and efficient. He kept me updated step by step and I'd highly recommend using him. I certainly will for my next purchase.Posted onTrustindex verifies that the original source of the review is Google. My mortgage needs were complex, but Lyndsey took the time to go through everything with care and professionalism. He explained my options clearly, guided me through each stage, and helped me secure the right mortgage. He always made himself available whenever I needed support. I’m extremely grateful for his help and would highly recommend West Wales Money.Posted onTrustindex verifies that the original source of the review is Google. Recently used West Wales Money to source a BTL Mortgage and the service was amazing, very professional, lots of communication and completed in record time, Will definitely use again 👍🏻Posted onTrustindex verifies that the original source of the review is Google. We simply wouldn't have been able to buy the house that we wanted without the solid, unbiased advice, provided to me by West Wales Money. Thoroughly recommended 👍Posted onTrustindex verifies that the original source of the review is Google. Lindsey was very helpful with our mortgage; we found him very efficient with his work. Besides, he is a very nice, polite, and friendly person. Lindsey made every effort to work things out for us, and we are very happy with the result. After all, I would highly recommend him to anyone. As a matter of fact, I have already suggested him to one of my friends.Posted onTrustindex verifies that the original source of the review is Google. Lyndsey was invaluable in getting our mortgage, finding the best deal, handing all the document requests and overcoming issues with the mortgage provider's IT system. He understands the particular requirements for business owners or the self-employed in applying for residential mortgages and we would certainly use West Wales Money again.Posted onTrustindex verifies that the original source of the review is Google. I cannot thank Lyndsey enough for all the help and support he has given me with my remortgage, taking the stress out of a very stressful situation for me. He did exactly what he said he was going to do, when he said he would do it. The whole process has been so easy and this is completely down to Lyndseys professional attitude and to ensure that he provides a bespoke service for all his clients. He certainly delivered on that front. Nothing was too much trouble, he explained things clearly and ensured that I was completely clear of what was required and the costs etc before proceeding. I would thoroughly recommend Lyndsey at West Wales Money, and know that I will certainly be using his company and expertise again in the near future. Thank you again for helping me to not only to secure a mortgage , but for taking the stress of paperwork from me and making the whole process so easy. I really do appreciate it.Posted onTrustindex verifies that the original source of the review is Google. I used West Wales Money to explore getting a mortgage for a small holding that I wanted to buy. Lyndsey was really professional, friendly and went above and beyond to help me to get the right product. Sadly, we didn’t buy the property in the end, however I wouldn’t hesitate to go back to Lyndsey when the time comes. Highly recommended to everybody.

⭐⭐⭐⭐⭐ Rated 5 stars – trusted by portfolio landlords. Genuine reviews from landlords, company directors and experienced property investors.

WHY SPV LANDLORDS STRUGGLE TO BORROW AS MUCH AS THEY SHOULD

Many landlords invest through an SPV expecting smoother borrowing and better tax efficiency. Instead, they find themselves offered less than expected — or declined altogether — without a clear explanation.

Lenders assess SPV applications very differently from personal buy-to-let. Stress testing, affordability assumptions, and internal lender models often restrict borrowing, even when rental income looks healthy and the portfolio is performing well.

This leaves many experienced landlords questioning their figures, injecting more capital than planned, or delaying growth — when the real issue isn’t the investment, but how the application has been structured and where it’s been placed.

This is where most SPV borrowing strategies quietly break down.

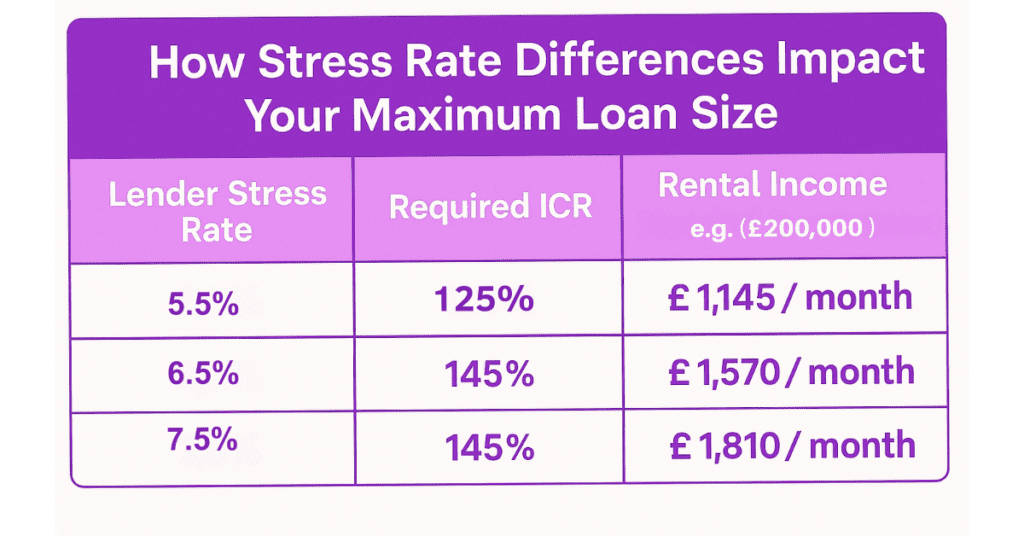

HOW LENDER STRESS TESTS AND ICR RULES RESTRICT SPV BORROWING

Many landlords run into problems because:

• Stress rates can be set as high as 7.5%, even if you’re fixing at a much lower rate

• ICR thresholds can reach 170–175%, requiring significantly higher rental income

• You’re asked to reduce borrowing or increase your deposit, even when the numbers feel strong

• Refinancing or expanding your portfolio starts to feel frustratingly out of reach

SECURE YOUR NEXT MORTGAGE BY GETTING ICR RIGHT

I work with landlords applying through SPVs or limited companies who want clear, strategic advice to overcome borrowing restrictions — particularly when it comes to the challenges of the ICR test.

I don’t just look at what lenders require. I take the time to understand your wider financial picture, so your mortgage is structured to satisfy lender criteria, optimise your tax position, and align with your long-term business goals — all in a way your accountant would approve of.

Whether you’re expanding your portfolio or refinancing existing properties, I’ll help you navigate complex lending rules with tailored solutions that make financial sense — not just now, but in the years ahead.

Specialist Lenders

Use SPV-friendly lenders with flexible stress testing to unlock higher borrowing potential

Limited Company BTL

Align SPV borrowing with accountant-approved tax strategies to support scalable growth

Complex Income

Present dividends, retained profits, and rental income clearly to avoid delays and rejections

TRUSTED BY LANDLORDS AND APPROVED BY ACCOUNTANTS

Real reviews from landlords who receive expert advice aligned with their accountant’s expectations

EXCELLENTTrustindex verifies that the original source of the review is Google. Lyndsey has been exceptional. Having a complicated case, Lyndsey was able to secure a mortgage for me. He kept me up to date throughout the whole process and has been extremely prompt with correspondence. Couldn't fault him at all. I highly recommend his services for anyone seeking a mortgage, especially those with extraordinary circumstances. Thank you very much.Posted onTrustindex verifies that the original source of the review is Google. Lyndsey (West Wales Money) helped me get a tricky mortgage deal through and was fast and efficient. He kept me updated step by step and I'd highly recommend using him. I certainly will for my next purchase.Posted onTrustindex verifies that the original source of the review is Google. My mortgage needs were complex, but Lyndsey took the time to go through everything with care and professionalism. He explained my options clearly, guided me through each stage, and helped me secure the right mortgage. He always made himself available whenever I needed support. I’m extremely grateful for his help and would highly recommend West Wales Money.Posted onTrustindex verifies that the original source of the review is Google. Recently used West Wales Money to source a BTL Mortgage and the service was amazing, very professional, lots of communication and completed in record time, Will definitely use again 👍🏻Posted onTrustindex verifies that the original source of the review is Google. We simply wouldn't have been able to buy the house that we wanted without the solid, unbiased advice, provided to me by West Wales Money. Thoroughly recommended 👍Posted onTrustindex verifies that the original source of the review is Google. Lindsey was very helpful with our mortgage; we found him very efficient with his work. Besides, he is a very nice, polite, and friendly person. Lindsey made every effort to work things out for us, and we are very happy with the result. After all, I would highly recommend him to anyone. As a matter of fact, I have already suggested him to one of my friends.Posted onTrustindex verifies that the original source of the review is Google. Lyndsey was invaluable in getting our mortgage, finding the best deal, handing all the document requests and overcoming issues with the mortgage provider's IT system. He understands the particular requirements for business owners or the self-employed in applying for residential mortgages and we would certainly use West Wales Money again.Posted onTrustindex verifies that the original source of the review is Google. I cannot thank Lyndsey enough for all the help and support he has given me with my remortgage, taking the stress out of a very stressful situation for me. He did exactly what he said he was going to do, when he said he would do it. The whole process has been so easy and this is completely down to Lyndseys professional attitude and to ensure that he provides a bespoke service for all his clients. He certainly delivered on that front. Nothing was too much trouble, he explained things clearly and ensured that I was completely clear of what was required and the costs etc before proceeding. I would thoroughly recommend Lyndsey at West Wales Money, and know that I will certainly be using his company and expertise again in the near future. Thank you again for helping me to not only to secure a mortgage , but for taking the stress of paperwork from me and making the whole process so easy. I really do appreciate it.Posted onTrustindex verifies that the original source of the review is Google. I used West Wales Money to explore getting a mortgage for a small holding that I wanted to buy. Lyndsey was really professional, friendly and went above and beyond to help me to get the right product. Sadly, we didn’t buy the property in the end, however I wouldn’t hesitate to go back to Lyndsey when the time comes. Highly recommended to everybody.

WHY LANDLORDS AND COMPANY DIRECTORS TRUST ME WITH COMPLEX SPV MORTGAGES

📞 Let’s Talk About Your SPV Strategy

Call: 07508 147884Hi, I'm Lyndsey!

When you’re arranging a mortgage through an SPV, small mistakes can have big consequences — reduced borrowing, higher tax, or stalled portfolio growth.

That’s why many landlords and company directors choose to work with me.

I provide specialist SPV mortgage advice for portfolio landlords across the UK and overseas. With over 30 years’ experience and access to specialist lenders, I help clients structure their borrowing to improve approval outcomes, optimise tax efficiency, and support long-term growth — all in a way their accountant would approve of.

You’ll deal directly with me throughout. I take the time to understand how lenders will assess your case, so your mortgage strategy is built on clarity, not guesswork.

My mission?

To help landlords structure SPV mortgages that borrow smarter, reduce friction, and support sustainable portfolio growth.

Real SPV Mortgage Success Stories: See What’s Possible

Case study 1: SPV mortgage for a portfolio landlord with complex income

👩💼 Client Profile:

A company director with a growing buy-to-let portfolio.

⚠️ The Challenge:

The client wanted to refinance multiple properties through a Special Purpose Vehicle (SPV) to make their borrowing more tax-efficient. However, they struggled to find a lender who would consider their income structure (a mix of salary and dividends) and the number of properties already held.

🔍 My Solution:

I worked closely with the client’s accountant to present their income in a way that aligned with lender affordability models. We used a lender that accepted SPV applications with no minimum income requirement and supported complex portfolios.

✅ Outcome:

✔ Successfully refinanced £750,000 across several properties.

✔ Secured a competitive fixed rate through the SPV.

✔ Reduced tax liability and positioned the client for future expansion.

💬 Client Testimonial:

“As a company director, I wasn’t sure I’d be able to borrow enough to secure the buy-to-let property I had my eye on. But with Lyndsey’s expert guidance and access to specialist lenders, I secured the higher borrowing I needed. I now own a solid investment property and have a clear strategy in place to grow my portfolio.”

Case Study 2: Smart SPV Mortgage for Tax-Efficient Portfolio Growth

👩💼 Client Profile:

Anthony – an experienced landlord with a portfolio of rental properties and income drawn from both property and limited company dividends.

⚠️ The Challenge:

Anthony wanted to refinance multiple properties through a Special Purpose Vehicle (SPV) to make his borrowing more tax-efficient. However, he struggled to find a lender who would consider his income structure (a mix of salary and dividends) and the number of properties already held.

🔍 My Solution:

I worked closely with Anthony’s accountant to present his income in a way that aligned with lender affordability models. We used a lender that accepted SPV applications with no minimum income requirement and supported complex portfolios.

✅ Outcome:

✔️ £200,000 capital released to fund the purchase of another property

✔️ Lower monthly repayments via a tailored interest-only setup

✔️ £1,200 monthly cash reserve created, improving liquidity

✔️ £2,500+ increase in monthly rental income from the new investment

✔️ A solid financial base to grow his portfolio further without over-leveraging

💬 Client Testimonial:

“Thanks to Lyndsey, he found a lender who worked with my circumstances and secured a remortgage that truly meets my needs!”

— Anthony, Experienced Landlord

The SPV Buy-to-Let Mortgage Guide

Created with accountant input to help landlords set up SPVs correctly from day one

What Happens When You Book a Discovery Call

How to Get SPV Mortgage Advice in Just 4 Simple Steps

📞 Step 1: Book Your Complimentary Mortgage Review

Send an enquiry and I’ll give you a call to understand your situation and what you’re looking to achieve.

📝 Step 2: I’ll Search Rates from Specialist Lenders

I compare fixed-rate deals across a wide panel of lenders — so you get a competitive rate that fits your needs and budget.

📝 Step 3: I’ll Handle the Application for You

No stress, no chasing forms — I take care of the paperwork and liaise with the lender on your behalf.

📦 Step 4: Relax While I Keep You Updated

You’ll receive regular updates throughout the process — all the way through to mortgage offer and completion.

Trusted Partners for Your Mortgage Needs

Discover Better Deals and Higher Borrowing Through Specialist Lenders

Accountant-Approved SPV Mortgage Advice — Built for Long-Term Growth

🏠 SPV Mortgage Expertise

Get one-to-one SPV buy-to-let mortgage advice tailored to your goals — with clear guidance, no jargon, and no pressure.

Book Your SPV Discovery CallWest Wales Money Ltd is registered with the Data Protection Act 2018 registration No ZA579253 and is authorised and regulated by the Financial Conduct Authority under Firm Reference No: 1005183 an Appointed Representative of TMG Direct Limited which is authorised and regulated by the Financial Conduct Authority under Firm Reference No: 786245 and registered with the Data Protection Act 1998 registration No: ZA178200.

YOUR HOME MAY BE REPOSSESSED IF YOU DO NOT KEEP UP REPAYMENTS ON YOUR MORTGAGE.

Think carefully before securing debts against your home. Your home may be repossessed if you do not keep up repayments on a mortgage or any other debt secured on it. The guidance and/or advice contained within this website is subject to the UK regulatory regime and is therefore targeted at consumers based in the UK.