Executive income protection is structured specifically for company directors who extract income through salary, dividends and retained profits. When illness interrupts that structure, the financial impact can be complex, layered and immediate.

Understanding that exposure is the first step toward protecting it properly.

What Happens If a Director Can’t Work for 6 Months?

What Happens If a Director Can’t Work for 6 Months?

As a company director, you’ve structured your income carefully.

You manage:

💷 Salary

📈 Dividends

🏢 Retained profits

📊 Tax efficiency

But if illness or injury stopped you working tomorrow, what actually happens?

Dividends usually stop

Business revenue may reduce

There’s no traditional employer sick pay

Your mortgage and personal commitments continue

For directors, income risk is layered.

And most directors only realise the exposure when income stops.

That is exactly why Executive Income Protection exists.

Executive Income Protection is a company-funded income protection arrangement designed specifically for limited company directors. It allows the business to insure a director’s income in a tax-efficient way, providing ongoing financial stability if illness or injury prevents them from working.

This structure differs from personal income protection because it integrates directly with company income, dividend extraction and corporate tax planning.

Why Standard Income Protection Often Fails Directors

Why Standard Income Protection Often Fails Directors

Most income protection plans are designed for salaried employees.

Directors are different.

Your income may include:

💼 PAYE salary

💰 Dividends

🔄 Irregular drawings

🧾 Retained company profits

Many off-the-shelf arrangements:

❌ Only cover basic salary

❌ Ignore dividend income

❌ Do not align with company structure

❌ Create tax inefficiencies

The problem?

These weaknesses only become visible at claim stage.

And that is the worst time to discover a structural mistake.

The Real Risk Directors Underestimate

The Real Risk Directors Underestimate

If you were unable to work:

Would dividends continue?

Would company profits remain stable?

Could your mortgage still be serviced?

Would savings begin to reduce?

Would retained profits erode faster than expected?

Many directors running limited company buy-to-let mortgages rely on dividend income to support affordability calculations. When that income is interrupted, pressure builds quickly — across both business and property commitments.

The real risk is not missing one month.

It is prolonged absence.

⏳ Recovery takes longer than expected.

📉 Business momentum slows gradually.

💷 Financial pressure increases steadily.

This is when strain compounds — personally, professionally and within the company itself.

Tax Benefits of Executive Income Protection

When structured properly:

📌 Premiums are usually treated as an allowable business expense

📌 The company receives corporation tax relief

📌 No P11D benefit in kind typically arises

📌 Benefits paid to the company are taxable

📌 Payments to you are treated as income

The net effect?

Often significantly more efficient than personal income protection alone.

But structure matters.

Personal vs  Executive Income Protection – What Is Right?

Executive Income Protection – What Is Right?

It is not always either/or.

It depends on:

🧾 How you extract income

📊 Your dividend structure

📈 Company profitability

🏠 Mortgage and personal commitments

🛡 Existing protection in place

For many directors, a blended approach provides the strongest outcome.

This is where specialist advice becomes important.

A Real-World Director Scenario

A Real-World Director Scenario

A director earning:

£12,570 salary

£70,000 dividends

Is signed off for 9 months.

Without structured protection:

❌ Dividends stop

❌ Salary alone is insufficient

❌ Savings reduce quickly

❌ Mortgage pressure builds

With Executive Income Protection:

✔ The company receives benefit

✔ Income continues

✔ Business stability improves

✔ Personal financial strain reduces

Same illness.

Completely different outcome.

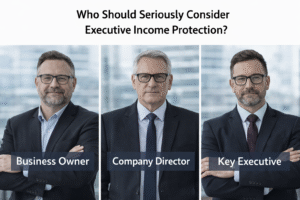

Who Should Seriously Consider Executive Income Protection?

Who Should Seriously Consider Executive Income Protection?

This is particularly relevant if you:

🔹 Are a limited company director

🔹 Extract income via dividends

🔹 Have a mortgage or long-term commitments

🔹 Are key to company revenue

🔹 Do not have substantial passive income

If the business depends on you, your income should be protected properly.

Why Specialist Advice Matters

Why Specialist Advice Matters

Executive Income Protection is not a comparison-site purchase.

Important structural decisions include:

📅 Deferred period

📏 Percentage of income insured

📑 Definition of incapacity

🏢 Ownership and company setup

🤝 Alignment with your accountant

🔄 Integration with other cover

Small structural errors can create significant inefficiencies.

The objective is not simply to “have cover”.

It is to design protection that integrates seamlessly with your:

Business

Tax strategy

Mortgage commitments

Long-term plans

Protecting Your Future Begins Today

Protecting Your Future Begins Today

You have structured your company carefully.

Your protection should be structured with the same precision.

A short conversation can clarify:

✔ Whether Executive Income Protection is appropriate

✔ How it should be positioned tax-efficiently

✔ What level of income should be protected

✔ How it integrates with your wider financial planning