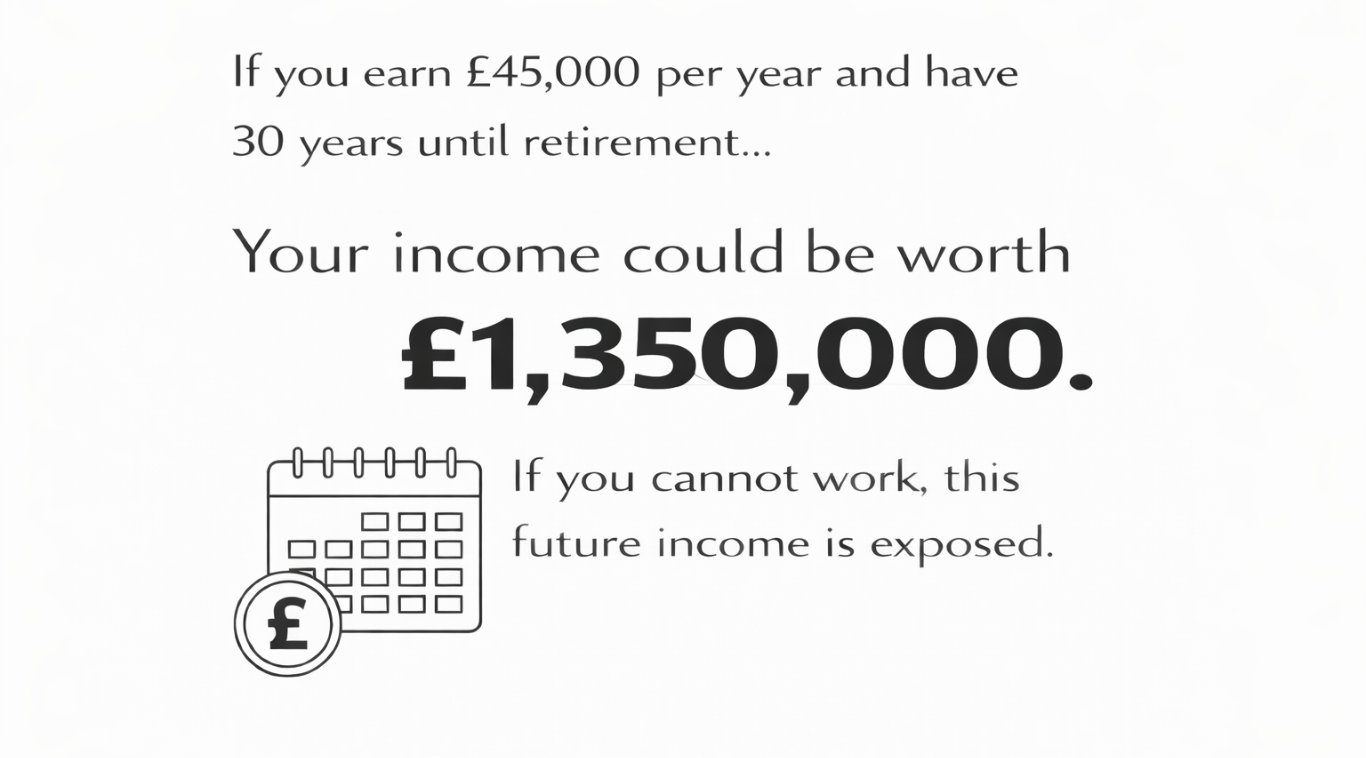

Your income is the engine behind everything you’ve built — your home, your lifestyle, your family’s security and your long-term plans. But what happens if illness or injury suddenly stops that income? Most people insure their car and their home, yet very few insure the one thing that pays for it all.

WHAT HAPPENS IF YOUR INCOME STOPS TOMORROW?

It’s not something we like to think about — but it’s worth considering calmly and realistically.

If you couldn’t work for several months:

-

Would your employer continue paying you?

-

How long would your savings last?

-

Could your household manage on one income?

-

Would your mortgage still be affordable?

For many people, the honest answer is: “We’d cope for a short while… but not for long.”

And most long-term sickness isn’t dramatic — it’s stress, back problems, mental health, or recovery from surgery.

THE FINANCIAL IMPACT NO ONE PLANS FOR

Statutory Sick Pay is limited — and for many self-employed individuals or company directors, it may not exist at all.

When your income stops, financial pressure can build fast — the mortgage, bills, daily expenses and credit commitments still need paying. It’s not just about money; it’s the stress of coping when your focus should be on getting better.

The financial pressure can build quickly:

- ⚠️ Mortgage repayments

- ⚠️ Household bills

- ⚠️ Food and daily expenses

- ⚠️ Childcare or school costs

- ⚠️ Loan or credit commitments

It’s not just about money — it’s about stress at a time when your focus should be recovery.

HOW INCOME PROTECTION ACTUALLY WORKS

Income Protection replaces a portion of your income if illness or injury prevents you from working.

In simple terms:

-

✅ You pay a monthly premium

-

✅ If you’re signed off work, the policy pays a regular monthly benefit

-

✅ Payments continue until you return to work or reach the end of the policy term

You can choose:

-

The level of cover

-

The waiting period before payments begin

-

How long benefits are paid

Modern policies are flexible and often include rehabilitation support to help you return to work safely.

WHY THIS IS EVEN MORE IMPORTANT FOR COMPANY DIRECTORS

WHY THIS IS EVEN MORE IMPORTANT FOR COMPANY DIRECTORS

If you are self-employed or a company director, you may not have the safety net of employer sick pay.

For directors taking income through a combination of salary and dividends, structuring Income Protection correctly is particularly important. Not all policies treat income the same way.

This is where proper advice matters — ensuring the cover reflects how you are actually paid.

WHO SHOULD SERIOUSLY CONSIDER INCOME PROTECTION?

WHO SHOULD SERIOUSLY CONSIDER INCOME PROTECTION?

Income Protection is particularly important if you:

🔸 Have a mortgage or long-term financial commitments

🔸 Are self-employed or a company director

🔸 Are the main earner in your household

🔸 Rely heavily on salary, bonuses or dividends

🔸 Have dependants

🔸 Do not have substantial savings

If your lifestyle depends on your income, this is a conversation worth having.

TAKE ADVICE RATHER THAN BUY ONLINE

TAKE ADVICE RATHER THAN BUY ONLINE

ncome Protection is not a “one size fits all” product.

The differences between policies can be significant — particularly around definitions of incapacity, deferred periods, exclusions and claim terms.

When I review Income Protection for clients, I consider:

-

Your employment structure

-

Your mortgage commitments

-

Your business position (if applicable)

-

Your long-term financial plans

The aim is simple:

Protection that works when it matters — not just a cheap premium.

FINAL THOUGHT: Protect the One Asset That Pays for Everything

FINAL THOUGHT: Protect the One Asset That Pays for Everything

You insure your car.

You insure your home.

But your income is the asset that funds it all.

Without it, everything else becomes vulnerable.

Income Protection isn’t about fear — it’s about resilience.

Reviewing your income Reviewing your income protection early gives you more options and greater control over your financial future — book your Protection Review today.